4.2 Solutions

- Load the quality of government dataset.

qog <- read.csv("https://raw.githubusercontent.com/QMUL-SPIR/Public_files/master/datasets/QoG2012.csv")- Rename the variable

wdi_gdpctogdpcusingrename()from thetidyverse. - Delete all rows with missing values on

gdpc. - Inspect

former_coland delete rows with missing values on it. - Turn

former_colinto a factor variable with appropriate labels. - Subset the dataset so that it only has the

gdpc,hdi, andformer_colvariables and sort the dataset byhdiusingarrange(), all in one ‘pipe’. - Plot the distribution of

gdpcconditional on former colony status, usingtheme_minimal(),labs()andscale_colour_discrete()to make sure your plot is clear and easy to understand. - Compute the probability that a country is richer than 55,000 per capita.

- Compute the conditional expectation of wealth for a country that is not a former colony.

- What is the probability that a former colony is 2 standard deviations below the mean wealth level?

- Compute the probability that any country is in the wealth interval from 20,000 to 50,000.

4.2.0.1 Exercise 1

Load the quality of government dataset.

qog <- read.csv("https://raw.githubusercontent.com/QMUL-SPIR/Public_files/master/datasets/QoG2012.csv")4.2.0.2 Exercise 2

Rename the variable wdi_gdpc to gdpc using rename() from the tidyverse.

library(tidyverse)

qog <- qog %>%

rename(gdpc = wdi_gdpc)4.2.0.3 Exercise 3

Delete all rows with missing values on gdpc.

# to check whether there are any missings or not

qog <- qog %>%

drop_na(gdpc)4.2.0.4 Exercise 4

Inspect former_col and delete rows with missing values on it.

# we instpect the variable and check for missings

summary(qog$former_col) Min. 1st Qu. Median Mean 3rd Qu. Max.

0.0000 0.0000 1.0000 0.6348 1.0000 1.0000 # no missing data!4.2.0.5 Exercise 5

Turn former_col into a factor variable with appropriate labels.

# we check the current storage type

str(qog$former_col) int [1:178] 0 0 1 1 1 0 1 0 0 1 ...# it's numeric (or 'integer'), so we change it to nominal

qog$former_col <- factor(qog$former_col,

levels = c(0,1),

labels = c("not colonised", "former colony" ))

# or we could pipe it

# qog <- qog %>%

# mutate(former_col = factor(former_col,

# levels = c(0,1),

# labels = c("not colonised", "former colony")))

# let's check the results

table(qog$former_col)

not colonised former colony

65 113 4.2.0.6 Exercise 6

Subset the dataset so that it only has the gdpc, undp_hdi, and former_col variables and sort the dataset by hdi using arrange(), all in one ‘pipe’.

qog <- qog %>%

select(gdpc,

undp_hdi,

former_col) %>%

arrange(gdpc)4.2.0.7 Exercise 7

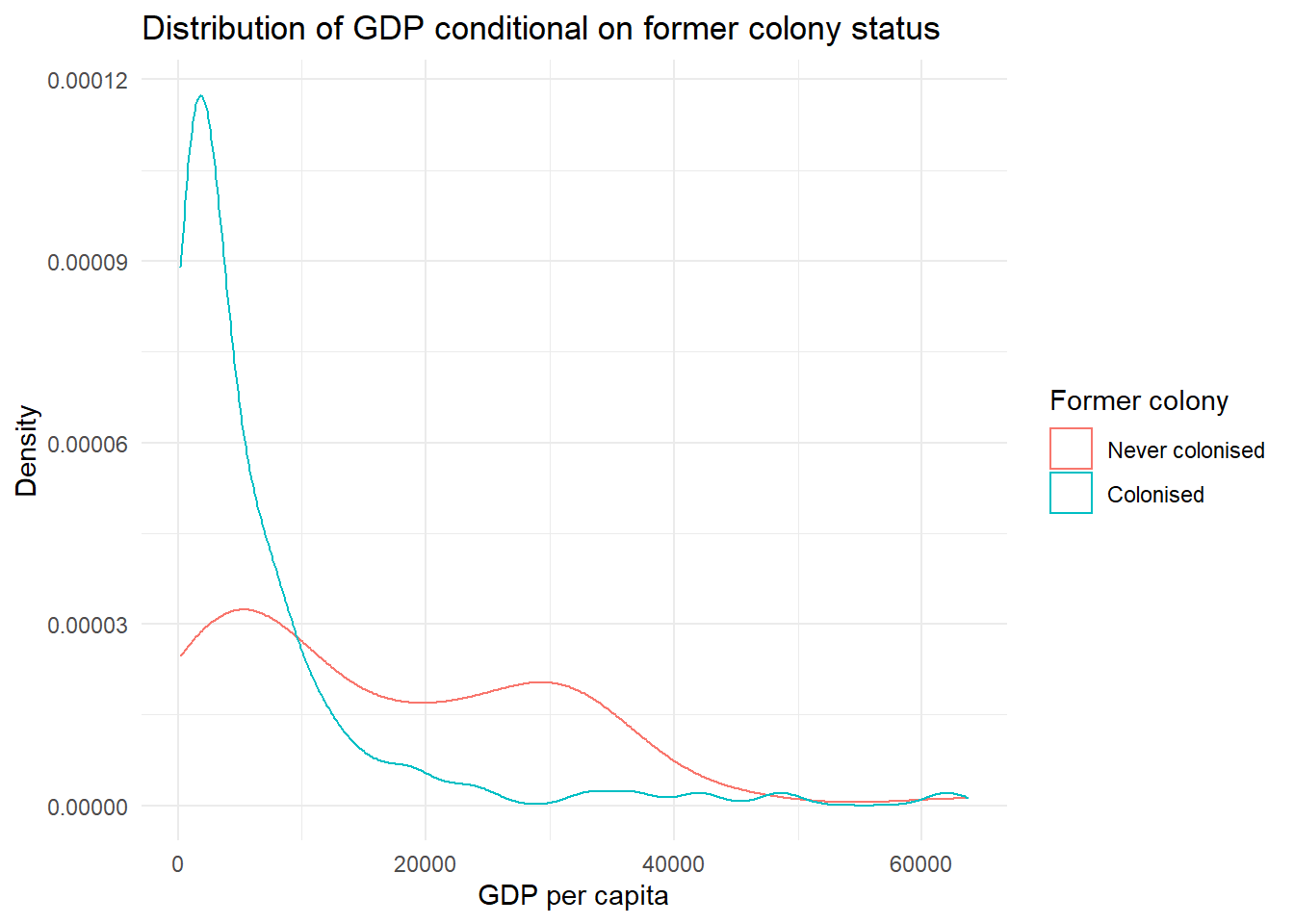

Plot the distribution of gdpc conditional on former colony status, using theme_minimal(), labs() and scale_colour_discrete() to make sure your plot is clear and easy to understand.

gg_gdpc <- ggplot(qog,

aes(gdpc,

group = former_col)) +

geom_density(aes(colour = factor(former_col))) +

labs(x = "GDP per capita", # clearer x axis label

y = "Density",

title = "Distribution of GDP conditional on former colony status") + # clearer y axis label

scale_color_discrete(name = "Former colony", # change legend title

labels = c("Never colonised", # change legend labels

"Colonised")) +

theme_minimal()

gg_gdpc

4.2.0.8 Exercise 8

Compute the probability that a country is richer than 55,000 per capita.

# get the empirical cumulative distribution of wealth

dist_wealth <- ecdf(qog$gdpc)

# probability

1 - dist_wealth(55000)[1] 0.01123596The probability is 0.01. Put differently 1 percent of countries are richer than 55,000 US dollars per capita.

4.2.0.9 Exercise 9

Compute the conditional expectation of wealth for a country that is not a former colony.

The conditional expectation is the mean of wealth among all former colonies.

# dataset of just non-former colonies

non_colonies <- qog %>%

filter(former_col == "not colonised")

# take mean of gdp

mean(non_colonies$gdpc)[1] 16415.39The conditional expectation of wealth for non-former colonies is approximately 17,250 US dollars per capita.

4.2.0.10 Exercise 10

What is the probability that a former colony is 2 standard deviations below the mean wealth level?

We first find out what the standard deviation and mean of wealth are in the conditional distribution of wealth for former colonies.

# dataset of just former colonies

colonies <- qog %>%

filter(former_col == "former colony")

# standard deviation of wealth for former colonies

sd_wealth_cols <- sd(colonies$gdpc)

sd_wealth_cols[1] 9783.914# but what is the mean?

mean_wealth_cols <- mean(colonies$gdpc)

mean_wealth_cols[1] 6599.714The standard deviation is greater than the mean. Apparently, former colonies are very different. Some do poorly and some extremely well. Negative wealth does not exist. Consequently, the answer is that there is 0 probability of a country having a gdp two standard deviations below the mean.

4.2.0.11 Exercise 11

Compute the probability that any country is the wealth interval from 20,000 to 50,000.

We compute the cumulative probabilities that a country has 20,000 and 50,000 and then take the difference.

# get the empirical cumulative distribution of wealth

dist_wealth_2 <- ecdf(qog$gdpc)

# cumulative probability of 20,000

p1 <- dist_wealth_2(20000)

# cumulative probability of 50,000

p2 <- dist_wealth_2(50000)

# probability of country in the interval

p2 - p1[1] 0.1741573The probability is approximately 0.17, so we expect about 17% of countries to fall in this interval.